Tadalafil gehört zur Gruppe der PDE5-Hemmer und wirkt über eine hochselektive Blockade des Enzyms Phosphodiesterase Typ 5. Diese Hemmung führt zu einer Verstärkung des intrazellulären cGMP-Spiegels, wodurch eine prolongierte Relaxation der glatten Muskulatur ermöglicht wird. Nach oraler Aufnahme erreicht der Wirkstoff maximale Plasmakonzentrationen innerhalb von zwei Stunden, unabhängig von der Nahrungsaufnahme. Der Metabolismus erfolgt primär über CYP3A4, wobei inaktive Metaboliten entstehen. Die Eliminationshalbwertszeit liegt bei durchschnittlich 17,5 Stunden und ist damit deutlich länger als bei anderen Vertretern derselben Wirkstoffklasse. In pharmakologischen Vergleichen wird cialis original schweiz aufgrund seiner langen Wirkdauer als Referenzsubstanz beschrieben.

Branimir.ws

University of Rome "Tor Vergata", Italy

We compare government investment and consumption multipliers in developed economies during

the recent …scal consolidation, following the Blanchard and Leigh (2013) approach. We …nd that,

in highly-indebted countries, the investment multiplier is likely to be much higher than what has

been assumed by policy makers and much higher than the consumption multiplier. This leads to the

conclusion that the consolidation should be accompanied by increased public investment.

Keywords: …scal consolidation, …scal multiplier, public consumption, public investment, public

Developed economies are currently going through a …scal consolidation. One of the main questions

for developed countries is how to design the consolidation in order to reduce the damage it will have

on growth (see Lagarde (2013)). To do that, activities with lower impact on growth should be reduced

more than activities with a greater impact.

The author would like to thank Alberto Zazzaro, Emanuele Brancati, Giovanni Callegari, Maddalena Cavicchi-

oli, Gerardo Manzo, Sabina Silajdzic and other participants at the 54th Annual Conference of the Italian EconomicAssociation, for very useful suggestions, and one anonymous referee for comments on an earlier version of the paper.

It is usually considered that government investment has a greater impact on growth (i.e., mul-

tiplier) than government consumption. For instance, the Golden Rule of public …nance states that

governments should borrow only for investment, not for consumption, since investment pays for itself,

through the future tax revenues generated by the new capital stock (Perotti (2004)). Some economists

have argued that the current …scal consolidation should allow some support through public invest-

ment. Christina Romer, for instance, argues: "There is simply no question that the United States

needs to enact a comprehensive plan for long-term de…cit reduction as soon as possible. But any such

plan could and should include another substantial dose of …scal expansion in the short run— ideally

one oriented toward public investment." (Romer (2012), p. 13). Similarly, Spilimbergo et al. (2008),

when advising on the appropriate …scal policy for the crisis, say: "(.) spending programs, from

repair and maintenance, to investment projects delayed, interrupted or rejected for lack of funding or

macroeconomic considerations, can be (re)started quickly" (Spilimbergo et al. (2008), p. 5).

Despite these recommendations, there is very scarce evidence that the government investment

multiplier is higher than the government consumption multiplier in the distressed economies. Hence, it

may not come as a surprise that the …scal authorities in these countries have ignored these suggestions.

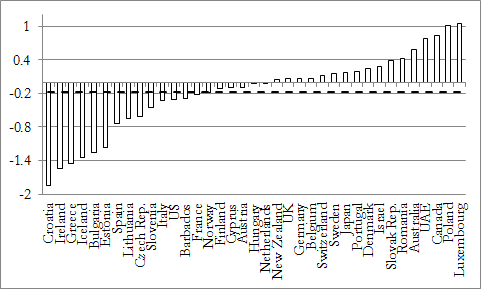

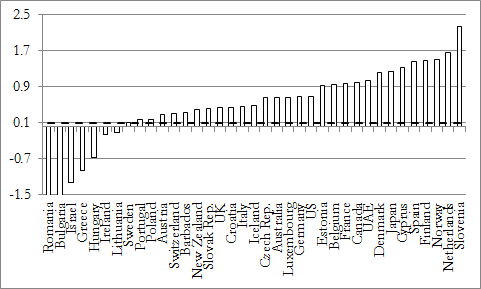

As a result, investment spending has been cut more than consumption expenditure during the on-

going consolidation (see Figure 1). In Greece, for instance, public investment in 2010 and 2011 has

been cut by 1.5 percent of Gross Domestic Product (GDP) (relative to the previous three years), while

public consumption has been cut by only 1 percent. In Ireland, similarly, investment has been cut by

1.5 percent of GDP, while consumption by only 0.2 percent. As a matter of fact, public investment

in 37 developed economies that we analyse1 , has been cut, on average, by 0.2 percent of GDP, while

public consumption has been increased by 0.1 percent of GDP2 (see section III on the data sources).

1. We analyse the countries that the World Bank classi…es as high-income, plus the EU countries that are still

low-income. See section III for more.

2. If the two outliers are excluded (Bulgaria and Romania, where consumption has fallen by 9 percent of GDP), the

average increase in public consumption is even higher, 0.6 percent.

Figure 1: Government investment (left) and government consumption (right)

Source: Author’s calculations, using data from Gwartney et al. (2012) and World Bank’s World Develop-

ment Indicators. The dashed lines are the averages for all the countries.

This paper will compare the government investment and the government consumption multiplier

in the advanced economies during 2011 and 2012. The approach that will be used is similar to that

of Blanchard and Leigh (2013) - growth forecast errors (the di¤erence between realised and expected

GDP growth) for 2011 and 2012 will be regressed on variables measuring government investment

and government consumption during the previous years, 2010 and 2011. Since the forecasts should

incorporate all the relevant information known at the time of their preparation, and the government

consumption and investment for the previous year were known when the forecasts for the forthcoming

year were prepared, the two should be uncorrelated if the right multipliers were used. If the coe¢ cients

on public consumption and investment turn out to be positive and signi…cant, that would imply that

the multipliers are higher than those that were assumed. The analysis will distinguish between the

highly-indebted and the non-highly-indebted countries, due to the conventional understanding that

the …scal multiplier may be lower, or even negative, in times of high debt.

The results point out that the consumption multipliers have been neither higher nor lower than

those assumed by the forecasters, both for the countries with high debt and for the countries with not-

so-high debt; same for the investment multipliers in the non-highly-indebted countries. However, the

investment multipliers in the highly-indebted countries seem to be substantially higher, by more than

one, than those that were assumed in the forecasts. Assuming that the consumption and investment

multipliers that were used in the forecasts are similar (a reasonable assumption, judging by Coenen

et al. (2012), p. 46, Table 3), these results suggest that the investment multiplier is much higher

than the consumption multiplier in the highly-indebted countries. Assuming that similar investment

multipliers were used for the highly-indebted and the not-so-highly-indebted countries, these results

suggest that the investment multiplier is higher in the former than in the latter.

The …nding that the investment multiplier is higher than the consumption multiplier reiterates

one of the basic postulates of Keynesian economics - that public investment is the best way for the

government to support the economy. Several explanations can be o¤ered for the higher investment

multiplier: public investment, besides the demand e¤ects, has also supply side e¤ects; public invest-

ment is less likely to crowd-out private demand, than public consumption; public investment is less

likely to end up in imports or savings, compared to public consumption.

The …nding that the investment multiplier is higher for the highly-indebted countries comes as

a surprise, however, since it is usually believed that high debt reduces the multiplier, through the

expectations e¤ect (higher probability for a default in the future). We o¤er two explanations for this

…nding. First, it may happen that the highly-indebted countries have a low level of public capital

(relative to the optimal level), which makes the return on public capital high (see Perotti (2004), for

a similar explanation, though in the opposite direction). Indeed, the …nding for the higher investment

multiplier is driven by countries considered as having weak public infrastructure - Greece, Ireland

and Italy. An alternative explanation is through an expectations e¤ect, but in an opposite direction

- if the public does not believe in austerity, i.e. expects the austerity to increase the public debt,

instead of decreasing it (which may happen if it expects a high multiplier), the expectations e¤ect

may add up to the standard Keynesian e¤ects. The possibility for this self-ful…lling outcome has

recently been discussed by Blanchard, Mauro and Dell’Ariccia (2013) and IMF (2013a). Support for

this explanation is found in existing studies on sovereign bonds dynamics, which …nd that markets

value GDP growth more than reduction in …scal de…cit (see Caggiano and Greco (2011), EC (2012b),

The strong interpretation of these …ndings is that by increasing government investment and cutting

government consumption more than proportionately, policy makers can achieve two goals at the same

time - reduce the de…cits and support the economy. The weak interpretation is that public investment

should be the last on the list for cutting during a consolidation.

The rest of the paper is structured as follows. Section II discusses the related literature, and

section III describes the methodology and the data. Section IV presents the basic results as well as

some robustness checks. Section V discusses the …ndings and section VI concludes.

Keynesian economics considers public investment as the most e¤ective …scal policy instrument

- it combines the short-run support of the government consumption with the long-term supply-side

bene…ts (see Skidelsky (2001)). The Golden Rule of …scal policy follows the same logic, and argues

that government investment can be …nanced by new debt, unlike government consumption, since it

will pay for itself, by the tax revenues from the new capital stock. However, there has been very

weak evidence in support of the claims that the government investment is more e¤ective for growth

than government consumption in the developed countries, in the period preceding the crisis. On

the contrary, Perotti (2004) shows that neither the short-run, nor the long-run multipliers from the

government investment spending are higher than the multipliers from government consumption, in

…ve developed countries (US, UK, Canada, Germany and Australia). His explanation for this …nding

is that developed countries have a high level of public capital, which makes its marginal product

low. Similarly, models used by leading world institutions assume similar multipliers from public

investment and public consumption. Coenen et al. (2012) compare the e¤ects of di¤erent forms of

…scal stimulus using seven Dynamic Stochastic General Equilibrium (DSGE) models used by leading

policy-making institutions, including the International Monetary Fund (IMF). They …nd that the

government investment spending has stronger e¤ects on the GDP than the government consumption,

but only marginally (see Table 3, p. 46).

The vast literature on …scal multipliers that has appeared during the crisis has not overlooked this

issue entirely. Eggertsson (2011) analyses which …scal policy is likely to be e¤ective in the current

situation, with zero lower bound and insu¢ cient demand, using a DSGE model. He …nds that a tem-

porary increase in government spending targeted at goods which are imperfect substitutes with private

consumption, like public infrastructure, is one of the most e¤ective measures. Auerbach and Gorod-

nichenko (2012b) compare the consumption and investment multipliers in the US, using a Smooth

Transition Vector Autoregression that allows the multipliers to di¤er in recessions and expansions.

They …nd that the investment multiplier is much higher than the consumption multiplier, particu-

larly in recessions (the cumulative investment multiplier in recessions is 4.3, while the corresponding

consumption multiplier is 1.3). They also …nd that the multipliers, in general, are likely to be much

larger in recessions than in expansions.

The dependence of the multiplier on the state of the business cycle has been analysed by other

researchers, too, like Batini, Callegari and Melina (2012), Baum, Poplawski-Ribeiro and Weber (2012)

and Caprioli and Momigliano (2013). All these papers apply a similar technique (regime-switching

Vector Autoregression) and arrive at similar conclusions - that the multipliers are likely to be greater

when the economy is in a downturn. The explanation is that in recessions, government spending is

less likely to crowd-out private spending.

Another strand of literature has investigated the relationship between the …scal multiplier and the

level of the public debt. The conventional wisdom argues that with a high level of public debt the

multiplier is likely to be lower, since the positive demand e¤ects are o¤set by negative expectations

e¤ect. Government spending increases the probability for a future tax hike, when the debt is high,

which reduces expected lifetime income, and hence - output. The recent literature investigating this

relation unanimously …nds that the level of debt reduces the multiplier; see Auerbach and Gorod-

nichenko (2012a), Ilzetzki, Mendoza and Vegh (2010), Kirchner, Cimadomo and Hauptmeier (2010),

Nickel and Tudyka (2013), and Rusnak (2011).

Because the current situation in most of the advanced economies is characterised both by a de-

pressed economy with zero interest rates and high public debt, it is not straightforward to assess the

size of the current multipliers, since the …rst attribute pushes for high multipliers, while the second

for low. Blanchard and Leigh (2013) investigate whether the multipliers that have been used by the

IMF and other professional forecasters recently have been correct or not. They use a simple, yet

very smart proposition - if the multipliers have been correct, there should be no correlation between

the growth forecast errors (the di¤erence between the realised and forecasted GDP growth) and the

planned …scal policy measures, since the planned measures have been taken into account when the

forecasts have been prepared. Thus, by regressing the growth forecast errors on the planned …scal

consolidation, one can assess whether the models that have been used for the forecasts are correct

or not. If one …nds signi…cant coe¢ cients for the planned consolidation, then that would imply that

the multipliers "assumed"3 in the models are incorrect. That is what Blanchard and Leigh (2013)

…nd - that the models have underestimated the multipliers, i.e. that the multipliers in the advanced

countries in the current situation are likely to be high.

3. Since the forecasts from the models are a result of many di¤erent factors, it is not entirely correct to speak about

certain values of multipliers assumed in the models. We will, nevertheless, use this word, for ease of exposition.

The methodology that is used in this paper is a modi…ed version of the approach by Blanchard

and Leigh (2013) and is based on regressing the growth forecast errors in a given year on variables

measuring …scal policy during the previous year. If the multipliers that were used for producing the

forecasts are correct, the growth forecast errors should be uncorrelated with government spending

from the previous year, since these data were known when the forecasts were prepared. Hence, a

regression of the growth forecast errors for year t on variables measuring …scal decisions made during

1 should produce insigni…cant coe¢ cients. If the coe¢ cients turn out to be signi…cant, that

would indicate that the e¤ect of the …scal decisions on the growth has been either overestimated (if

the coe¢ cients are negative) or underestimated (if the coe¢ cients are positive).

We extend the analysis of Blanchard and Leigh (2013) in two ways. First, instead of using a measure

of the overall …scal stance, we will distinguish between government consumption and government

investment, in order to evaluate the proposals for supporting the economy through public spending4 .

Second, we will allow the multipliers to di¤er for the highly indebted countries, given the widespread

belief that the multipliers are lower, or even negative, when the debt is high. Therefore, our basic

+ 2*Government Investmentt 1;i+ 3*Government Consumptiont 1;i*High Public Debtt 1;i

+ 4*Government Investmentt 1;i*High Public Debtt 1;i + t;i

where the subscript t indexes the years 2011 and 2012 and i indexes the countries. The analysis

will be done on a sample of developed countries, since it is these countries that are going through

…scal consolidation. To end up with as many observations as possible, we select the countries that

the World Bank classi…es as high income economies, plus the EU countries that are still not high

income, on which there are the required data. As will become clear, results are almost identical when

various versions of restricted samples (like the advanced economies of the IMF) are used. Hence,

the following 37 countries are included: Australia, Austria, Barbados, Belgium, Bulgaria, Canada,

Croatia, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary,

Iceland, Ireland, Israel, Italy, Japan, Lithuania, Luxembourg, Netherlands, New Zealand, Norway,

4. The third component of public spending, the public transfers, are excluded from the analysis, due to data unavail-

Poland, Portugal, Romania, Slovak Republic, Slovenia, Spain, Sweden, Switzerland, United Arab

Emirates, United Kingdom, United States. Since certain data is unavailable for 2012, 62 observations

in total will be analysed. This may seem low, but it should be noted that similar studies work with

an even lower number of observations (e.g., the baseline regression of Blanchard and Leigh (2013) is

The forecast errors for the GDP growth are calculated as a di¤erence between the realised real

GDP growth in year t (2011 and 2012) and the projected growth for that year at the beginning of year

t. Projected GDP growth is taken from the April editions of the World Economic Outlook (WEO)

in year t; i.e. 2011 and 2012 (IMF (2011) and IMF (2012)). These projections are prepared at the

beginning of the year, when all the relevant data for the previous year are known, including the …scal

stimulus, but economic growth for the current year is still unknown. GDP growth and public debt is

from the April 2013 edition of the WEO (IMF (2013b)).

Government consumption is de…ned as the di¤erence between the government consumption in year

t 1 (2010 and 2011) and the average government consumption for 2007-2009. Government investment

is de…ned analogously. We take the di¤erence from the average for the period 2007-2009, instead of

from a value for a single year (e.g. 2009), to avoid potential base e¤ects - since GDP in 2009 in many

of these countries was lower than usual, due to the recession, the share of government consumption

and investment in GDP may have been higher than usual in 2009, which may overestimate the …scal

High public debt is a dummy variable which takes value of one for countries with gross5 public

1 (2010 and 2011). Five countries have debt above 95% in

2010: Belgium, Greece, Italy, Japan and US, and three more in 2011 - Iceland, Ireland and Portugal.

The 95% threshold is chosen after Baum, Checherita-Westphal and Rother (2013). All in all, 11 of

the 62 observations can be classi…ed as “high debt” episodes (Iceland and Ireland drop out due to

unavailability of data on GDP growth for 2012 in the April 2013 WEO).

Data on government consumption are from the World Development Indicators (WDI) database

of the World Bank. Data on government investment are calculated from Gwartney, Lawson and

Hall (2013a), who, in their Economic Freedom of the World database, provide data on government

investment as a share of total investment for about 130 countries. The sources of the government

investment data in this database are: Government Finance Statistics Yearbook of the IMF; WDI

5. We take the gross debt, instead of the net, since the latter is available for fewer countries.

of the World Bank; International Finance Statistics of the IMF; World Economic Forum, Global

Competitiveness Report; United Nations National Accounts; and Transition Indicators of European

Bank for Reconstruction and Development (see Gwartney, Lawson and Hall (2013b) p. 236). These

values are then multiplied with the share of gross …xed capital formation in the GDP, from WDI.

The results of the main regression are presented in Table 1, column 1. All the variables in the

regression are insigni…cant, except the cross-product of the high debt dummy and the government

investment, which is signi…cant at the 1% level. The insigni…cance of the government consumption and

government investment variables points out that the multipliers implied in the forecasts are unlikely

to di¤er from the actual ones, for the countries without high debt. The insigni…cance of the cross

product of the government consumption with the high debt dummy indicates that there are likely no

di¤erences between the consumption multipliers for the highly-indebted and the non-highly-indebted

countries, assuming that similar multipliers were used for them in the forecasts. On the other hand,

the cross-product of the high debt dummy and the government investment is signi…cant at the 1% level.

The sum of this coe¢ cient with the government investment coe¢ cient gives the di¤erence between

the investment multiplier implied in the forecasts and the actual one, for the countries with high debt.

The sum is signi…cant at the 1% level, again, indicating that the actual investment multiplier for

the highly indebted countries is likely to be higher than the one used in the forecasts by around 1.7.

Assuming that similar investment multipliers were used for the highly-indebted and the non-highly-

indebted countries, this suggests that the investment multiplier is higher for the indebted countries.

Furthermore, if the impact of government consumption and investment on GDP was assumed to be

similar in the indebted countries, this implies that the investment multiplier is likely to be higher than

the consumption multiplier in these countries. Evidence from Coenen et al. (2012) suggest that this is

likely to be the case - they examine the growth e¤ects of government consumption and investment in

the main workhorse models of the leading policy institutions in the world, …nding that the investment

multiplier is only marginally higher than the consumption multiplier.

In the next two columns of Table 1, we check whether the results change if the sample of countries

is changed. In column 2, we estimate the regression for the group of countries that the World Bank

classi…es as high income (i.e. we exclude the EU countries which are still low income). In this way,

we lose 6 observations, compared to the initial regression. In column 3, we restrict the sample to the

countries that the IMF classi…es as advanced, losing 6 additional observations. As can be seen, the

results remain very similar - the cross product of the high debt and the government investment is

always signi…cant at one percent, as well as its sum with the government investment. Therefore, we

continue the analysis with the initial group of countries, due to the highest number of observations in

We next explore the possibility that our results are driven by certain outliers. In column 4, we

estimate the equation using quantile regression, which uses the median of the variables, instead of

the mean. In column 5, we estimate the equation using the robust regression technique of Andersen

(2008). The variable of interest has a slightly lower coe¢ cient in these two regressions, but remains

signi…cant (at the 5% level). In column 6, we bootstrap the standard errors in the baseline regression,

due to the small sample size6 . The variable of interest remains signi…cant, though only at the 10%

Table 1: Baseline results and some sensitivity analysis

Dependent variable in all regressions is the growth forecast error.

p-values in parentheses. ***, ** and * denote signi…cance at 1%, 5% and 10%, respectively.

6. The bootstrapping exercise was done using 3000 replications. Higher number of replications gave similar results.

The seed used for the simulation in Stata was 26011982, the date of birth of the author.

Next, we add certain controls in the baseline regression. It is possible that certain factors, cor-

related with the growth forecast error and the …scal support, may be driving the results, like some

factors that push for expansionary …scal policy and higher than expected growth at the same time.

By including additional controls, we also, in a certain way, control for possible errors in the forecasts

regarding the e¤ects of the other variables on the GDP. We start by adding the trade and …nancial

‡ows experienced in year t (exports, FDI and portfolio ‡ows; see Table 8 in the appendix for a de…n-

ition of these variables and the other variables from this section). Unexpected ‡ows, caused by …scal

decision from the previous year, may bias the results. Column 2 of Table 2 shows these results. They

are almost the same as the baseline. In column 3, we add the monetary policy stimulus during year

1, by including the interest rate and the expansion of the M1. If both the monetary and …scal

policy are expansionary, and the forecasters have underestimated the e¤ect of the monetary policy

on growth, then the signi…cance of the …scal variables may be capturing the e¤ect of the monetary

policy. This does not seem to be the case, since the monetary policy variables are insigni…cant and

the …scal policy variables remain unchanged. In column 4, we add certain variables for the banking

system - the share of capital in the total assets and the share of non-performing loans in year t

These variables are likely to be correlated with the …scal policy, due to the bank bailouts, for instance,

and if their e¤ect on GDP growth has not been well accounted for, then the signi…cance of the …scal

variables may be due to their omission. Again, this does not seem to be the case. Next, we include the

level of public debt and the …scal balance in year t

1 - high debt (or de…cit) may be correlated with

the …scal policy, and is likely to a¤ect growth, too. The results remain unchanged, again. Next, we

include the current account balance - external imbalance may be related to …scal policy (twin de…cits)

and may a¤ect growth at the same time. However, the results remain stable once again.

The …scal decisions may be endogenous with respect to the growth forecast errors through another

channel - through political factors. Certain factors of political nature may lead to lower than expected

GDP growth and may be correlated with the …scal decisions from the previous year. For instance,

political instability, or inability to reach agreement in the parliament, are likely to a¤ect the size of the

stimulus/consolidation, as well as its design (the allocation between consumption and investment).

They may also lead to lower growth than initially expected. To control for this, we add several

variables capturing certain political characteristics. We include: 1) a dummy for coalition governments

- coalition governments are more di¢ cult to reach an agreement for decisive cuts in government

spending; 2) a dummy for control of all the relevant houses - if the party in power has control of

all the relevant houses, it can implement problematic cuts or reforms more easily; 3) the share of

seats in the parliament belonging to the government parties - the bigger the share of seats in the

parliament belonging to the government parties, the more easily the government will make politically

problematic decisions; 4) a dummy for left orientation of the government - parties on the left of the

political spectrum may be more reluctant to cuts in government spending. These data are taken from

the Database of Political Institutions 2012 of Beck et al. (2001). The results are presented in column

7 of Table 2. As can be seen, the variable of interest remains signi…cant, though only at 10%.

Dependent variable in all regressions is the growth forecast error.

p-values in parentheses. ***, ** and * denote signi…cance at 1%, 5% and 10%, respectively

In order to see if the results are driven by certain countries, we next do a simulation in which we

randomly discard twelve observations (20% of the sample), and reestimate the baseline regression on

the remaining 50 observations.7 We repeat this exercise six times. The results, shown in Table 3,

yield additional support to our …ndings.

Table 3: Randomly discarding 20 percent of the sample

Dependent variable in all regressions is the growth forecast error.

p-values in parentheses. ***, ** and * denote signi…cance at 1%, 5% and 10%, respectively.

As yet another check, we estimate the baseline regression eliminating each of the countries one

by one. Table 4 presents these results. As can be seen, the coe¢ cient of interest is always highly

signi…cant (p-value around 0.01) and with a similar magnitude as in the baseline regression (around

1.7), except in the case when Greece is excluded, when it becomes insigni…cant. Being at the heart of

the sovereign debt crisis, it is not strange to …nd that Greece drives the results. The growth forecast

errors for Greece have been much higher than for any other country. In addition, two of the eleven

high-debt observations belong to Greece. Because of this, we believe that it would be incorrect to

7. The seed that was used for generating the random samples in Stata is 26011982.

Note: The table presents the coe¢ cient of interest (gov.inv + high debt*gov.inv.) and

its p-value when the baseline regression is estimated

As an additional robustness check, we do a Bayesian Model Averaging (BMA) exercise, by which

we try to see which of the discussed explanatory variables is likely to be the most robust determinant

of the growth forecast errors. BMA is appropriate for situations when a large number of candidate

explanatory variables exists, and the researcher does not know a priori what the correct theoretical

model is. It estimates all the possible model combinations, using Bayesian techniques, weights them

according to their goodness of …t, and calculates the weighted average for every variable. Inference

in BMA is normally based on the Posterior Inclusion Probability (PIP), which is the probability that

the variable is a robust determinant of the dependent variable. For a thorough elaboration of BMA,

see Hoeting et al. (1999), or for a short applied exposition, see Jovanovic (2012). The BMA results

are shown in Table 5. We use four di¤erent priors for the model coe¢ cients (benchmark prior, unit

information prior (UIP), hyper prior, and empirical Bayes local prior (EBL)8 ). For the model size,

8. The benchmark prior has been proposed by Fernandez, Ley and Steel (2001), the UIP prior by Kass and Wasserman

(1995), the EBL prior by Hansen and Yu (2001), and the hyper prior by Liang et al. (2008).

we use the dilution prior suggested by Durlauf, Kourtellos and Tan (2008), which is an extension of

the dilution prior proposed by George (1999). This prior is used in situations when multicollinearity

may be a problem (see Feldkircher (2012), for example), because it penalises models which include

variables with high correlation. We use this prior because three pairs of variables appeared highly

collinear in our case, with correlation exceeding 0.7 (see Table 9 in the appendix). It should be noted

that very similar results are obtained with other model priors. Each column of Table 5 presents results

obtained with one of the model coe¢ cients prior. All the results are based on the 500 best models.

For clarity, we will present only the PIPs, the other statistics are available upon request.9

Government consumption * High public debt

The …gures in the table are the Posterior Inclusion Probabilites (PIP).

* indicates variables with PIP above 0.5 (signi…cant variables).

The only two signi…cant variables in all the estimations are the exports and the cross product

of the high debt dummy and the government investment. Therefore, it can be said that the results

9. The BMA analysis has been implemented in R, using the BMS library, developed by Feldkircher and Zeugner

of the BMA analysis con…rm the previous …ndings, that the government investment is likely to be a

signi…cant determinant for the explanation of the growth forecast error in the indebted countries.

We also check whether the results hold when the IMF forecasts are replaced with forecasts from

other institutions. Table 6, column 1 shows the results with forecasts from the European Commission,

while column 2 shows the results when the forecasts from Consensus Economics are used.10 The …nd-

ings for the public investment remain as before. We also check if the correlation between the forecast

errors and public investment is a rule rather than an exception. Column 3 of Table 6 shows the results

of the baseline regression for developing countries, while column 4 shows the results of the regression

for developed countries, but during "good times", i.e. for the period before the …nancial crisis (2007

and 2008). As can be seen, all the …scal variables are insigni…cant in these two regressions, pointing

out that the IMF forecast errors are likely to be random, normally, and that the correlation between

the public investment and the growth forecast errors is present only for the developed countries, dur-

ing the consolidation. Last, we replace the growth forecast errors with the GDP growth, and add the

forecasted GDP growth as an additional regressor (column 5, Table 6). The forecasted GDP appears

highly signi…cant, with a coe¢ cient of 1.16, indicating that the realised GDP is indeed correlated with

the forecasts. The variable of interest retains its magnitude, but loses the signi…cance (the p-value is

0.12), which can be attributed to its correlation with the additional regressor.

10. The spring forecasts from the European Commission are used EC (2011) and EC (2012a)), and the April editions

of the Consensus Economics forecasts for G7 and Western Europe and Eastern Europe (ConsensusEconomics (2011a),ConsensusEconomics (2011b), ConsensusEconomics (2012a), ConsensusEconomics (2012b)).

Table 6: Other forecasts, periods and countries

Dependent variable in the …rst four regressions is the growth forecast error, in the …fth, it is the GDP growth.

p-values in parentheses. ***, ** and * denote signi…cance at 1%, 5

Two main messages should be taken from this analysis. The …rst one is that public investment

is likely to have a bigger impact on GDP in the indebted countries, than public consumption. Our

study is not the only recent study to suggest that the investment multiplier is likely to be higher

than the consumption multiplier - Auerbach and Gorodnichenko (2012b) also …nd that the investment

multiplier is much larger than the consumption multiplier (for example, in recessions, their consump-

tion multiplier is 1.4, while the investment multiplier is 4.3). This …nding is by no means novel, and

can be explained in several ways. The …rst explanation is through the supply-side e¤ects - public

investment, in addition to the main demand e¤ect, increases the capital stock, i.e. the potential GDP.

However, this e¤ect is unlikely to be the main driving force behind our results, since this e¤ect primar-

ily refers to the long run. A second explanation may be the smaller crowding out of the government

investment. Government investment is usually focused on goods which are imperfect substitutes with

private consumption, therefore, they are unlikely to crowd out private expenditure (see Eggertsson

(2011), for instance). Third, public investment has fewer "leakages" than public consumption - it is

more labour-intensive, so less likely to end up in imports than public consumption (see Spilimbergo,

Symansky and Schindler (2009), p. 2-3).

The second message from the analysis is that, contrary to the widespread belief, the (investment)

multiplier is likely to be higher in the highly-indebted countries, than in the not-highly-indebted ones.

We propose two possible explanations. . The …rst one is that the indebted countries may have, at the

same time, a low level of public capital (relative to the optimal level), as a result of which its marginal

product is high. Similar logic, though in the opposite direction, is proposed by Perotti (2004), in his

…ndings that the investment multiplier does not di¤er from the consumption multiplier in the US,

UK, Canada, Germany and Australia (the argument there is that these countries may have too high

a level of capital, which makes the investment multiplier low).

To check how likely this explanation is, we divide the highly-indebted countries in our sample

into two groups: countries with a high level of public capital and countries with a low level of public

capital. We use the quality of overall infrastructure from the Executive Opinion Survey of the Global

Competitiveness Report as a proxy for public capital (WEF (2011), p. 412). In particular, in the

high public capital group, we include Iceland, Portugal, Japan, Belgium and the US, while in the

low capital group - Ireland, Greece and Italy.11 Then, we estimate the baseline regression, restricting

the sample of high-debt countries only to those with high-capital (Table 7, column 2), and only to

those with low-capital (Table 7, column 3). It can be seen that when only the high-capital high-

debt countries are included, we no longer …nd evidence that the multipliers di¤er. On the other

hand, when the low-capital high-debt countries are included, our previous …ndings regarding the

higher investment multiplier in the highly-indebted countries remain. Hence, we may say that the

explanation for the higher investment multiplier in the indebted-countries through the low public

capital, and, consequently high marginal product on it, is supported by the data.

11. The index covers three aspects of the infrastructure - transport, telephony and energy. It covers around 140

countries. The highest possible value of the index is 7, the lowest 1. The average value of the index in 2010-11 for thewhole world is 4.3. However, as only Italy has a value lower than this average, we choose 5 as the cut-o¤ point for highvs. low public capital. The US, the lowest ranked high-capital country has a value of 5.7 and is ranked 24th in theworld. Ireland, the highest ranked low-capital country, has a value of 4.6 and is ranked 53rd.

Table 7: Checking the public capital explanation

Dependent variable in all regressions is the growth forecast error.

p-values in parentheses. ***, ** and * denote signi…cance at 1%, 5% and 10%, respectively

Another explanation for the higher investment multiplier in the highly-indebted countries is through

the con…dence e¤ects. Con…dence e¤ects are usually used to justify non-Keynesian e¤ects of …scal

expansion and are the basis of "the German view" on …scal policy (Giavazzi and Pagano (1990), p.

76). Hellwig and Neumann (1987), p.137-138, for instance, say: "The direct demand impact of slower

public expenditure growth is clearly negative. (.) The indirect e¤ ect on aggregate demand of the

initial reduction in expenditure growth occurs through an improvement in expectations if the measures

taken are understood to be part of a credible medium-term program of consolidation" (see also Fels

and Froehlich (1987)). Blanchard (1990) proposes a model in which …scal consolidation increases

consumption. The idea is that by undertaking consolidation today, the government eliminates the

need for larger, probably more disruptive consolidation in the future, which increases the expected

lifetime income of households, and hence consumption. Baxter and King (1993) analyse, through

a model, under which circumstances …scal expansions can produce a negative response in economic

activity, …nding that this is likely to happen when the expansion is …nanced by taxes, since they in-

crease the expected future tax burden. Sutherland (1997) and Perotti (1999) develop models in which

…scal policy has standard, Keynesian e¤ects under low debt, but switches to non-standard e¤ects as

the level of debt becomes high.12 What all these models have in common is that the non-standard

e¤ects emerge from some form of the wealth e¤ect - …scal contraction reduces the probability for

a future increase in taxes, as a result of which the expected lifetime income increases, which raises

consumption. Non-Keynesian e¤ects can emerge through a slightly di¤erent source, too, as discussed

in Giavazzi, Jappelli and Pagano (2000). If the …scal policy stance is unsustainable, it may lead, if not

corrected, to public debt repudiation and severe output losses. Fiscal contraction in such cases reduces

the probability of default, which would have a¤ected output adversely. As a result, the expected net

lifetime income rises, leading to an increase in current private consumption. Miller, Skidelsky and

Weller (1990) propose a model with a similar reasoning - there is a critical level of public debt above

which the government imposes a tax on bond holders. As the level of debt increases, the rate on

government bonds rises to re‡ect the increased risk of the tax being imposed. The increased interest

rate crowds out private spending. Fiscal contraction then, in a situation when the debt is high, is

expected to reduce the debt, hence the probability that the tax will be imposed, hence the interest

But, suppose that, in a situation when the debt is high, agents expect that contractionary …scal

policy will increase the debt. Why would this happen? If agents perceive that the multiplier is greater

than one, then they would expect that cutting public spending will decrease the GDP more than it will

decrease the debt, as a result of which the debt-to-GDP ratio will increase further. The interest rate

on government bonds will then rise, to re‡ect the higher probability of default. In such a situation,

the con…dence e¤ects may add up to the Keynesian e¤ects, resulting in a greater multiplier when

the debt is higher, contrary to the conventional belief. Hence, if agents believe that the multiplier

is high, then this may indeed lead to a higher multiplier, when the debt is high. If agents believe

that the investment multiplier is higher than the consumption multiplier, and if the consolidation

is implemented mainly through cuts in public investment, this explanation is likely to hold only for

investment spending, not necessarily for consumption.

The possibility for these self-ful…lling multiple equilibria has recently been discussed by Blanchard,

Mauro and Dell’Ariccia (2013), p. 12, and IMF (2013a), p. 21. Support for this explanation is found

in existing studies on sovereign bonds dynamics, which …nd that markets value GDP growth more

12. Bertola and Drazen (1993) also develop a model in which the relationship between …scal policy (government

consumption as a share of GDP) and private consumption (as a share of GDP) is non-linear, depending on the level ofdebt. However, in their model the relationship is negative when the debt is low and positive when the debt is high.

than reduction in …scal de…cit. Romer (2012) …nds that bad news about growth is the second most

important factor driving increases in the Spanish government bond rate in the period April 2011-April

2012, after news about the response to the European crisis. The analysis in EC (2012b), p.35, also

points out that …nancial markets may indeed prefer GDP growth to …scal adjustment - sovereign

spreads are found to react much stronger to expected GDP growth than to changes in …scal balance.

Similar results are found in Caggiano and Greco (2011).

The existing literature (Auerbach and Gorodnichenko (2012a), Ilzetzki, Mendoza and Vegh (2010),

Kirchner, Cimadomo and Hauptmeier (2010), Nickel and Tudyka (2013), Rusnak (2011)), …nds that

the …scal multiplier is lower when the debt is high. Our …ndings about the higher multiplier in the

highly-indebted countries is not necessarily at odds with these studies, because these studies actually

exclude the recent consolidation. The shocks in Auerbach and Gorodnichenko (2012a) end in 2008 or

2009 (see Figure 3), the data in Ilzetzki, Mendoza and Vegh (2010) end in 2009 (see Tables A1 and

A2), the data in Kirchner, Cimadomo and Hauptmeier (2010) end in 2008Q4, while those of Nickel

Bearing in mind that our results are driven by one country, Greece, it may be worthwhile to

consider certain alternative explanations for the association between the government investment and

the growth forecast errors. Bi, Qu and Roaf (2012), for instance, argue that the high forecast errors

for Greece are due to the overestimated potential output for Greece, not due to the underestimated

…scal multiplier. Their explanation is not in contrast with ours, however. Public investment can a¤ect

output both through the potential output and through the output gap. Hence, potential output may

have been overestimated exactly because the e¤ects of the cuts in public spending on the potential

What are the implications of these …ndings? If one strongly believes in them, i.e. if the investment

multiplier is really that higher than the consumption multiplier, that would suggest that by cutting

public consumption and increasing public investment less than proportionately, one can, at the same

time, lower the budget de…cit and stimulate growth. However, the results may be imprecisely estimated

for such a strong interpretation - there are only 62 observations. Also, the multiplier is likely to be

di¤erent for every country, so, the averages we estimate do not have to hold for every analysed country.

The weaker interpretation is, thus, that since the investment multiplier in the indebted countries is

likely to be higher than the consumption multiplier, the public investment should come last on the

list for cutting, as Alesina and Perotti (1997) argued some time ago. This has not been the practice

during the recent consolidation, as was shown on Figure 1. As can be seen there, public investment

was cut in 20 of the 37 countries, while consumption - in only 7.

Fiscal consolidation has dominated discussions among researchers and policy makers, recently.

With this paper, we join the discussion, o¤ering some new evidence on the size of the govern-

ment consumption and investment multipliers, in the highly-indebted and the less-indebted advanced

economies. We …nd evidence that the investment multiplier is likely to be higher than the consumption

multiplier, and the multiplier assumed by the policy-makers, in the highly-indebted countries. We put

through two possible explanations. First, the highly indebted countries may have at the same time

low level of public capital, which would make its marginal product high. Second, in a situation where

the highly indebted economies are depressed, with interest rates at the zero lower bound, markets may

assume that the …scal multiplier in them is high. Hence, they may expect that …scal consolidation

will increase the public debt to GDP ratio, instead of decreasing it, because GDP will fall more than

the reduction in de…cit. This would increase the probability to default and the sovereign bond rates,

which may adversely a¤ect output. Consequently, the expectations e¤ects may add up to the Key-

nesian e¤ects and result in a higher multiplier in the indebted countries. Whatever the explanation,

the results have important implications for the design of the consolidation. They suggest that the

consolidation should be accompanied by increased public investment.

Alesina, Alberto, and Roberto Perotti. 1997. “Fiscal Adjustments In OECD Countries: Com-

position and Macroeconomic E¤ects.” IMF Sta¤ Papers, 44: 210–248.

Andersen, Robert. 2008. Modern Methods for Robust Regression. Thousand Oaks, California. Auerbach, Alan, and Yuriy Gorodnichenko. 2012a. “Fiscal Multipliers in Recession and Ex-

pansion.”In Fiscal Policy after the Financial Crisis. , ed. Alberto Alesina and Francesco Giavazzi. University of Chicago Press.

Auerbach, Alan, and Yuriy Gorodnichenko. 2012b. “Measuring the Output Responses to Fiscal

Policy.” American Economic Journal - Economic Policy, 4(2): 1–27.

Batini, Nicoletta, Giovanni Callegari, and Giovanni Melina. 2012. “Successful Austerity in

the United States, Europe and Japan.”International Monetary Fund IMF Working Paper 12/190.

Baum, Anja, Cristina Checherita-Westphal, and Philipp Rother. 2013. “Debt and growth:

New evidence for the euro area.” Journal of International Money and Finance, 32(C): 809–821.

Baum, Anja, M. Poplawski-Ribeiro, and A. Weber. 2012. “Fiscal Multipliers and the State

of the Economy.” International Monetary Fund IMF Working Paper, Washington DC.

Baxter, Marianne, and Robert G. King. 1993. “Fiscal Policy in General Equilibrium.”American

Beck, Thorsten, George Clarke, Alberto Gro¤, Philip Keefer, and Patrick Walsh. 2001.

“New tools in comparative political economy: The Database of Political Institutions.” WorldBank Economic Review, 15(1): 165–176.

Bertola, Giuseppe, and Allan Drazen. 1993. “Trigger Points and Budget Cuts: Explaining the

E¤ects of Fiscal Austerity.” American Economic Review, 83(1): 11–26.

Bi, Ran, Haonan Qu, and James Roaf. 2012. “Assessing the Impact and Phasing of Multi-year

Fiscal Adjustment: A General Framework.” International Monetary Fund IMF Working Paper,Washington DC.

Blanchard, Olivier J. 1990. “Comments on Giavazzi and Pagano.” In NBER Macroeconomics

Annual 1990. , ed. Olivier Blanchard and Stanley Fischer, 110–117. Cambridge, MA:MIT Press.

Blanchard, Olivier J., and Daniel Leigh. 2013. “Growth Forecast Errors and Fiscal Multipliers.”

American Economic Review, 103(3): 117–120.

Blanchard, Olivier J., Paolo Mauro, and Giovanni Dell’Ariccia. 2013. “Rethinking Macro

Policy II: Getting Granular.”International Monetary Fund IMF Sta¤ Discussion Note No. 13/03,Washington DC.

Caggiano, Giovanni, and Luciano Greco. 2011. “Sovereign Risk in the Euro Area: Is it Mostly

Caprioli, Francesco, and Sandro Momigliano. 2013. “The E¤ects of Expenditure Shocks in Italy

During Good and Bad Times.” In Public Debt, Global Governance and Economic Dynamism. ,ed. L. Paganetto, 213–232. Springer.

Coenen, Gunter, Christopher Erceg, Charles Freedman, Davide Furceri, Michael

Kumhof, Douglas Laxton Rene Lalonde, Jesper Linde, Annabelle Mourougane, DirkMuir, Susanna Mursula, John Roberts, Werner Roeger, Carlos de Resende, StephenSnudden, Mathias Trabandt, and Jan in’t Veld. 2012. “E¤ects of Fiscal Stimulus in Struc-tural Models.” American Economic Journal: Macroeconomics, 4(1): 22–68.

ConsensusEconomics. 2011a. Eastern Europe Consensus Forecasts April 2011. Consensus Eco-

ConsensusEconomics. 2011b. G7 and Western Europe April 2011. Consensus Economics. ConsensusEconomics. 2012a. Eastern Europe Consensus Forecasts April 2012. Consensus Eco-

ConsensusEconomics. 2012b. G7 and Western Europe April 2012. Consensus Economics. Durlauf, S., A. Kourtellos, and C. Tan. 2008. “Are Any Growth Theories Robust?” Economic

EC, European Commission. 2011. “European Economic Forecast Spring 2011.”EC, European Commission. 2012a. “European Economic Forecast Spring 2012.”EC, European Commission. 2012b. Quarterly Report on the Euro Area 4/2012. European Union. Eggertsson, Gauti B. 2011. “What Fiscal Policy is E¤ective at Zero Interest Rates?” In NBER

Macroeconomics Annual 2010, Volume 25. NBER Chapters, 59–112. National Bureau of EconomicResearch, Inc.

Feldkircher, Martin. 2012. “The Determinants of Vulnerability to the Global Financial Crisis 2008

to 2009: Credit Growth and Other Sources of Risk.”Bank of Finland, Institute for Economies inTransition BOFIT Discussion Papers 26/2012.

Feldkircher, Martin, and Stefan Zeugner. 2009. “Benchmark Priors Revisited: On Adaptive

Shrinkage and the Supermodel E¤ect in Bayesian Model Averaging.” International MonetaryFund IMF Working Papers 09/202.

Fels, Gerhard, and Hans-Peter Froehlich. 1987. “Germany and the World Economy: A German

View.” Economic Policy, 2(4): 177–195.

Fernandez, C., E. Ley, and M. F. Steel. 2001. “Benchmark Priors for Bayesian Model Averag-

ing.” Journal of Econometrics, 100(2): 381–427.

George, E. I. 1999. “Discussion of Bayesian Model Averaging and Model Search Strategies by M.A.

Clyde.” Bayesian Statistics 6, 175–177.

Giavazzi, Francesco, and Marco Pagano. 1990. “Can Severe Fiscal Contractions Be Expansion-

ary? Tales of Two Small European Countries.”In NBER Macroeconomics Annual 1990, Volume5. NBER Chapters, 75–122. National Bureau of Economic Research, Inc.

Giavazzi, Francesco, Tulio Jappelli, and Marco Pagano. 2000. “Searching for Non Linear

E¤ects of Fiscal Policy: Evidence From Industrial and Developing Countries.”European EconomicReview, 44(7): 1259–1289.

Gwartney, James, Robert Lawson, and Joshua Hall. 2013a. “2013 Economic Freedom

Dataset.” Fraser Institute Economic Freedom of the World: 2013 Annual Report. available at:http://www.freetheworld.com/datasets_efw.html.

Gwartney, James, Robert Lawson, and Joshua Hall. 2013b. Economic Freedom of the World:

Hansen, M., and B. Yu. 2001. “Model selection and the principle of minimum description length.”

Journal of the American Statistical Association, 96(454): 746–774.

Hellwig, M., and M. J. M. Neumann. 1987. “Economic policy in Germany: Was there a

turnaround?” Economic Policy, 2(5): 105–140.

Hoeting, J. A., D. Madigan, A. E. Raftery, and C. T. Volinsky. 1999. “Bayesian Model

Averaging: A Tutorial.” Statistical Science, 14(4): 382–417.

Ilzetzki, Ethan, Enrique G. Mendoza, and Carlos A. Vegh. 2010. “How Big (Small?) are

Fiscal Multipliers?” Journal of Monetary Economics, 60(2): 239–254.

IMF, International Monetary Fund. 2011. World Economic Outlook: Tensions from the Two-

Speed Recovery: Unemployment, Commodities and Capital Flows. Washington DC:InternationalMonetary Fund. April.

IMF, International Monetary Fund. 2012. World Economic Outlook: Growth Resuming, Dan-

gers Remain. Washington DC:International Monetary Fund. April.

IMF, International Monetary Fund. 2013a. “Reassessing the Role and Modalities of Fiscal

IMF, International Monetary Fund. 2013b. World Economic Outlook: Hopes, Realities, and

Risks. Washington DC:International Monetary Fund. April.

Jovanovic, Branimir. 2012. “How policy actions a¤ect short-term post-crisis recovery?” CEIS Tor

Vergata CEIS Tor Vergata Working Paper 253.

Kass, R., and L. Wasserman. 1995. “A reference Bayesian test for nested hypotheses and its

relationship to the Schwarz criterion.” Journal of the American Statistical Association, 90: 928–934.

Kirchner, Markus, Jacopo Cimadomo, and Sebastian Hauptmeier. 2010. “Transmission of

Government Spending Shocks in the Euro Area - Time Variation and Driving Forces.”EuropeanCentral Bank ECB Working Paper 1219.

Lagarde, Christine. 2013. “Welcoming Remarks by the Managing Director.” International Mone-

tary Fund Rethinking Macro Policies II Conference.

Liang, F., R. Paulo, G. Molina, M. A. Clyde, and J. O. Berger. 2008. “Mixtures of g Priors

for Bayesian Variable Selection.” Journal of the American Statistical Association, 103: 410–423.

Miller, Marcus, Robert Skidelsky, and Paul Weller. 1990. “Fear of De…cit Financing: Is it

Rational?” In Public Debt Management: Theory and History. , ed. Draghi M. Dornbusch, R. Cambridge University Press.

Nickel, Christiane, and Andreas Tudyka. 2013. “Fiscal Stimulus in Times of High Debt: Re-

considering Multipliers and Twin de…cits.” European Central Bank ECB Working Paper 1513.

Perotti, Roberto. 1999. “Fiscal Policy in Good Times and Bad.”Quarterly Journal of Economics,

Perotti, Roberto. 2004. “Public investment: another (di¤erent) look.”Romer, Christina. 2012. “Fiscal Policy in the Crisis: Lessons and Policy Implications.”

Rusnak, Marek. 2011. “Why Do Government Spending Multipliers Di¤er? A Meta-Analysis.”Skidelsky, Robert. 2001. John Maynard Keynes: Fighting for Britain, 1937-1946. MacMillan

Spilimbergo, Antonio, Steve Symansky, and Martin Schindler. 2009. “Fiscal Multipliers.”

International Monetary Fund IMF Sta¤ Position Note 09/11, Washington DC.

Spilimbergo, Antonio, Steve Symansky, Olivier J. Blanchard, and Carlo Cottarelli. 2008.

“Fiscal policy for the crisis.”International Monetary Fund IMF Sta¤ Position Note 08/01, Wash-ington DC.

Sutherland, Alan. 1997. “Fiscal crises and aggregate demand: can high public debt reverse the

e¤ects of …scal policy?” Journal of Public Economics, 65(2): 147–162.

WEF, World Economic Forum. 2011. The Global Competitiveness Report 2011 - 2012. Geneva,

Table 8: Definitions of the additional variables used in the analysis

Exports of goods and services in 2011 and 2012, as % of GDP, minus average

Foreign direct investment, net in‡ows, in 2011 and 2012, as % of GDP, minus

Portfolio Investment, net incurrence of liabilities (excluding exceptional …nanc-

ing) in 2011 and 2012, as % of GDP, minus the average for 2007-2010. The

original data is in USD, so it is divided by the nominal GDP.

Monetary aggregate M1 (’money’ series in WDI), in 2010 and 2011, as % of

GDP, minus the average for 2007-2009 . The original series is in local currency

units, so it is divided by the nominal GDP.

The discount rate of the central bank in 2010 and 2011, minus the average for

Bank capital to asset ratio in 2010 and 2011.

Bank nonperforming loans to total loans in 2010 and 2011.

General government gross public debt in 2010 and 2011, % of GDP.

General government structural balance in 2010 and 2011, % of potential GDP.

Current account balance in 2010 and 2011, % of GDP.

Dummy if the ruling party had a control over all the parliament houses (name

Dummy if the ruling party was from the left side of the political spectrum

Share of parliament seats held by the government (name of variable in DPI:

Horizon Pharma Announces FDA Approval of DUEXIS® (ibuprofen/famotidine) for the Relief of the Signs and Symptoms of Rheumatoid Arthritis and Osteoarthritis and to Decrease the Risk of Developing Upper Gastrointestinal Ulcers NORTHBROOK, Ill. – April 25, 2011 – Horizon Pharma, Inc., a biopharmaceutical company developing and commercializing innovative medicines to ta

Rodrigo Andrés Riveros Miranda Instructor Asociado. Escuela de Psicología UC Jefe de Tecnologías de Apoyo, CEDETI-UC E-mail: [email protected] - Teléfono: (56-2) 3541776 Educación 2006 – 2007 UNIVERSITY OF BIRMINGHAM. Birmingham, UK Master of Research in Cognitive Neuropsychology and Rehabilitation. Graduado con Méritos Supervisores: Prof. Jane Riddoch & Dr. Jacqueline Snow

Figure 1: Government investment (left) and government consumption (right)

Source: Author’s calculations, using data from Gwartney et al. (2012) and World Bank’s World Develop-

ment Indicators. The dashed lines are the averages for all the countries.

Figure 1: Government investment (left) and government consumption (right)

Source: Author’s calculations, using data from Gwartney et al. (2012) and World Bank’s World Develop-

ment Indicators. The dashed lines are the averages for all the countries.