Tadalafil gehört zur Gruppe der PDE5-Hemmer und wirkt über eine hochselektive Blockade des Enzyms Phosphodiesterase Typ 5. Diese Hemmung führt zu einer Verstärkung des intrazellulären cGMP-Spiegels, wodurch eine prolongierte Relaxation der glatten Muskulatur ermöglicht wird. Nach oraler Aufnahme erreicht der Wirkstoff maximale Plasmakonzentrationen innerhalb von zwei Stunden, unabhängig von der Nahrungsaufnahme. Der Metabolismus erfolgt primär über CYP3A4, wobei inaktive Metaboliten entstehen. Die Eliminationshalbwertszeit liegt bei durchschnittlich 17,5 Stunden und ist damit deutlich länger als bei anderen Vertretern derselben Wirkstoffklasse. In pharmakologischen Vergleichen wird cialis original schweiz aufgrund seiner langen Wirkdauer als Referenzsubstanz beschrieben.

Novartis first half 2001 background slides

Investor Relations Background Information Half Year 2001 Results August 2001 Overview Solid Growth Trend in Pharmaceuticals Drives Group Sales Sales: CHF 15.5 bn, +12% in local currencies, +11% in CHF Sales growth in % (LC) Sales by region in % Pharmaceuticals Asia/Australia/ Generics1 Consumer Health CIBA Vision1 Rest of the Americas Animal Health 1Including acquisition benefits First Half Operating Income up 7% to CHF 3.5 bn Operating income1 growth Operating income by sector4 in % (CHF) Pharmaceuticals Pharmaceuticals Generics2 Consumer Health CIBA Vision3 Generics 4% Animal Health Consumer Animal CIBA Health Vision -35% -25% -15% -5% 5% 15% 1 Continuing activities 2 Including acquisition effects 3 Including Wesley Jessen integration costs of CHF 31 m 4 Excluding corporate and other expenses Group Operating Margin Lowered due to Significant Investments in Pharmaceutical Marketing & Sales 23.4 22.5 Generics Consumer ceuticals 1 Excluding exceptionals associated with Wesley Jessen of CHF 31 m Highlights Half Year 2001

•Major Approvals/ − Femara® 1st line in US Launches: − Starlix® in US and EU − Zometa® in EU for HCM − Gleevec™/Glivec® in > 10 countries − Foradil® in US − Riamet® in EU − Visudyne™ in EU for expanded use

•Delays: − Zelmac®/Zelnorm™ − Xolair®

•Filings: − Diovan® in US (priority review) and EU for heart failure − Glivec® in EU and Japan − Elidel™ in EU for atopic eczema Key Financials Sustained Growth First Half 2001 Key Figures for Continuing Activities Operating income as a % of sales 22.5 23.4 Net income as a % of sales 24.1 24.3 EPS (CHF) Free cash flow as a % of sales 0.7 2.2 Number of employees Sales Growth First Half 2001 Driven by Volume and Acquisitions Acq./Div. Currency Operating Costs – Increased Marketing to Support Product Launches and Expansions H1/2001 CHF m Change in % in CHF Cost of goods sold Marketing & Distribution Research & Development General & Administration Operating income -20% -10% Strong Balance Sheet – Debt/Equity Ratio 21% Liquid funds of CHF 15.1 bn Debt/Equity Ratio Dec-1999 Jun-2000 Dec-2000 Jun-2001 Net liquidity of CHF 7.3 bn Dec-1999 Jun-2000 Dec-2000 Jun-2001 Dec-1999 Jun-2000 Dec-2000 Jun-2001 Pharmaceuticals Pharmaceuticals – Continued Strong Growth

•Pharmaceutical sales posted 13% growth (in LC) driven by in- market products (Diovan®, Lotrel®, Lamisil®, Exelon®)

•Continued strong performance coming from US business with 21% growth (in LC)

•Excluding Famvir®/Denavir® and the transfer of Ophthalmic to Pharmaceuticals, growth would have been (in LC) 10% world-wide 15% in US Pharmaceuticals Top 20 Products I Total Sales Growth Total sales in CHF m Growth in % first half Sandimmun®/Neoral® Diovan®/Co-Diovan® Cibacen®/Lotensin® of which Lotrel® Aredia® Lamisil® Voltaren® Sandostatin® Miacalcic® Lescol® Tegretol® 1 Corrected for inter-sectorial transfers Pharmaceuticals Top 20 Products II Total Sales Growth Total sales in CHF m Growth in % first half Leponex®/Clozaril® Estraderm® (group) Exelon® Foradil® Famvir® /Denavir® Visudyne® Nitroderm TTS® Zaditen® Parlodel® Desferal® 1 Corrected for inter-sectorial transfers 15 2 Includes Meri range & Estalis Sandimmun®/Neoral® – Slow Generic Erosion in US 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 Sandimmun®/Neoral® Warfarin TRx Erosion % 50% Azathioprine Note: Month 1 is May 2000 Diovan® – On Its Way to Share Leadership in US US Category NRx Share:

•First half 2001 w-w sales: % Jan. 1998 to June 2001 CHF 806 m, +53% LC (US: +40% LC)

•Continues to outpace the ARB market segment (+47% w-w)

•On track to take category Losartan 36.7% leadership position in US: NRx share at 34.2%

•Recently published MARVAL trial Diovan® 34.2% demonstrates efficacy in microal- buminuria

•Only ARB to show CHF benefits; sNDA filed in April 2001 – priority review received in June (US) Source: IMS Health, NPA weekly, NRx share in ARB segment Lotrel® – Strong Continued Growth +47% Growth in First Half 2001 Lotrel® vs Amlodipine New Prescription Share (in %)

• First half ‘01 sales: CHF 346 m, +47% LC

• Significantly outpaced competition

• Patent extension to 2017 1 According to internal data Source: IMS Health, NPA Plus, NRx share in amlodipine segment Novartis Has the Two Fastest Growing Brands in the Top 10 Anti-Hypertensives in the US Product June NRx (MAT-IMS) % Growth 1. Norvasc 2. Zestril/Zestoretic 3. Prinivil/Prinzide 5. Toprol-XL 4. Accupril/Accuretic 6. Cozaar/Hyzaar 7. Diovan/Diovan HCT 3.68 m 39.6% 8. Lotensin/Lotensin HCT 3.36 m -0.5% 9. Monopril/Monopril HCT 10. Lotrel* 2.29 m 46.4% *Lotrel has just recently entered the top ten list Lamisil® Expanded Leadership Position1

•CHF 624 m, +18% in LC

•DTC campaign launched Lamisil Oral DTC campaign launched

•Labeling change in US Sporanox negatively affected Q2 sales 40%

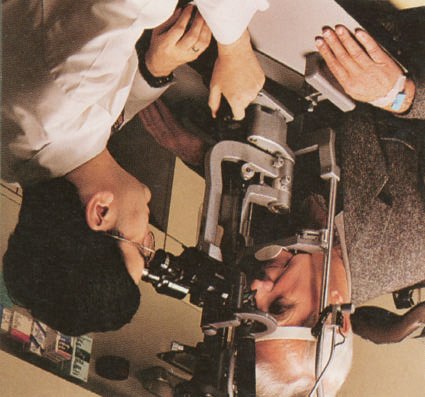

•Expansion of segment leadership Jan 98 Jul 98 Jan 99 Jul 99 Jan 00 Jul 00 Jan 01 Source: IMS Health, NPA Plus, 1 NRx share in Onychomycosis segment Trileptal® – Most Successful Anticonvulsant NRx Volume (000s) Trileptal® Neurontin Lamictal Zonegran Gabitril Months on the market 9 10 11 12 13 14 15 Source: IMS NPA; 5-15-01 Exelon® – Strong Share Position Alzheimer’s Disease: Exelon® Total Rx Share in US (in %) Source: IMS NPA Plus 7/TRx monthly VisudyneTM – Record Breaking Launch 2001 • First half sales CHF 178 m • Reimbursement in most countries

• Expanded reimbursement in EU • Indication for pathologic myopia

− Approved in EU in March 2001 − FDA approvable letter Launches and Brand Expansions

•Gleevec™/Glivec®

− Beat expectations with CHF 58 m in sales

− Positive recommendation in Europe, launch expected in Q4

•Femara®

− Market segment share gains, US NRx share 34% in June 01

− CHF 92 m, +64% in LC

•Starlix® US NRx trend flat

•Foradil®

− Significantly beaten Beta-2 market segment growth with +24% in LC

− Launched in US (May), targeting specialists Pharmaceutical Pipeline >20031 Starlix® ElidelTM ZelnormTM 2/Zelmac® Zometa® Certican® Zomaril® Foradil® GleevecTM/Glivec® GleevecTM/Glivec® J Lamisil® Foradil® US Apligraf® EU OctreoTherTM Tinea capitis Estalis® Ritalin® LA Osteoporosis Femara® GleevecTM/Glivec® Foradil® Diovan® Zometa® Bone met. Lamisil® Syst. myc. Co-Diovan® Xolair® 4 High dose ZelnormTM 2/Zelmac® NME roll-out LCM indication ZelnormTM 2/Zelmac® 1 Major projects only ZelnormTM 2/Zelmac® 2 Timing subject to result of appeal 3 Out-licensed to Speedel, call back option for Novartis Diovan® 4 Subject to further discussion with health authorities Appendix First Half 2001 Sales Growth Components by Sector Acq./Div. Currency Pharmaceuticals Generics Consumer Health CIBA Vision Animal Health Sales 2nd Quarter 2001 by Sector Growth in % Q2 2001 Q2 2000 Pharmaceuticals Generics Consumer Health CIBA Vision Animal Health Continuing activities Development of Major Currencies Against CHF Average rates Average rates first half 2001 first half 2000 Sales Performance of Recently Launched Pharmaceutical Products H1 Sales in CHF m Comtan® Femara® Gleevec™ Starlix® Trileptal® Zometa® Pharmaceuticals Top 20 Products Sales Performance First Half 2001 Pharmaceuticals Top 20 Products I US Sales Growth US Sales in CHF m LC Growth first half Sandimmun®/Neoral® Diovan®/Co-Diovan® Cibacen®/Lotensin® of which Lotrel® Aredia® Lamisil® Voltaren® Sandostatin® Miacalcic® Lescol® Tegretol® Pharmaceuticals Top 20 Products II US Sales Growth US Sales in CHF m LC Growth first half Leponex®/Clozaril® Estraderm® Exelon® Foradil® Famvir® /Denavir® Visudyne® Nitroderm TTS® Zaditen® Parlodel® Desferal® Pharmaceuticals Top 20 Products I RoW Sales Growth RoW Sales in CHF m LC Growth first half Sandimmun®/Neoral® Diovan®/Co-Diovan® Cibacen®/Lotensin® of which Lotrel® Aredia® Lamisil® Voltaren® Sandostatin® Miacalcic® Lescol® Tegretol® Pharmaceuticals Top 20 Products II RoW Sales Growth RoW Sales in CHF m LC Growth first half Leponex®/Clozaril® Estraderm® Exelon® Foradil® Famvir® /Denavir® Visudyne® Nitroderm TTS® Zaditen® Parlodel® Desferal® Pharmaceuticals Top 20 Products I Market segment Sandimmun®/Neoral® Transpl., RA, Psoriasis Diovan®/Co-Diovan® Hypertension Cibacen®/Lotensin® Antihypertensives Aredia® Oncology (Bone) Lamisil® Fungal infections Voltaren® Antirheumatics Sandostatin® Acromegaly Miacalcic® Osteoporosis Lescol® Cholesterol reduction Tegretol® Epilepsy Pharmaceuticals Top 20 Products II Market segment Leponex®/Clozaril® Schizophrenia Exelon® Alzheimer’s disease Estraderm® Hormone replacement Foradil® Asthma, Bronchitis Famvir® Acute herpes zoster Visudyne® Pathologic myopia Nitroderm TTS® Angina pectoris Zaditen® Asthma, Allergy Parlodel® Parkinson’s Desferal® Oncology/hematology

Office of the Minister of State Services Chair Cabinet Committee on State Sector Reform and Expenditure Control Future monitoring of the Accident Compensation Corporation and Housing New Zealand Corporation Proposal This paper outlines a recent decision by relevant Ministers to transfer monitoring of the Accident Compensation Corporation (ACC) and Housing New Zealand Corporation (HNZC)

GPCA Health Committee INFLAMMATORY BOWEL DISEASE (IBD) - 2011 OVERVIEW: This is a group of diseases of the small and large intestine, characterized by chronic and protracted diarrhea, malabsorption, weight loss, anemia, and malnutrition. They are all treatable, but seldom cured. In each specific disease, a different type of inflammatory cell is found in large numbers in the l

Group Operating Margin Lowered due to Significant

Group Operating Margin Lowered due to Significant VisudyneTM – Record Breaking Launch

VisudyneTM – Record Breaking Launch